My Psychiatrist gave me a Superbill. What is that?

A simple guide to understanding superbills and getting reimbursed for out-of-network psychiatry.

As a psychiatrist who’s been practicing for many years now, I always have patients complain about being confused with what is a superbill and often struggle to navigate that with their insurance company. Why do I have to pay if I have insurance? What’s this sorcery? So the goal of this is to help you get some clarity and understand what a Superbill is. For this example, I will be a private psychiatrist – meaning – I don’t work with any insurance companies when seeing patients and they have to pay the fees before the appointment. In the previous article, I talk about how this makes me an Out-of-Network provider for them. And, every time they see me, I give them a Superbill to submit to their insurance.

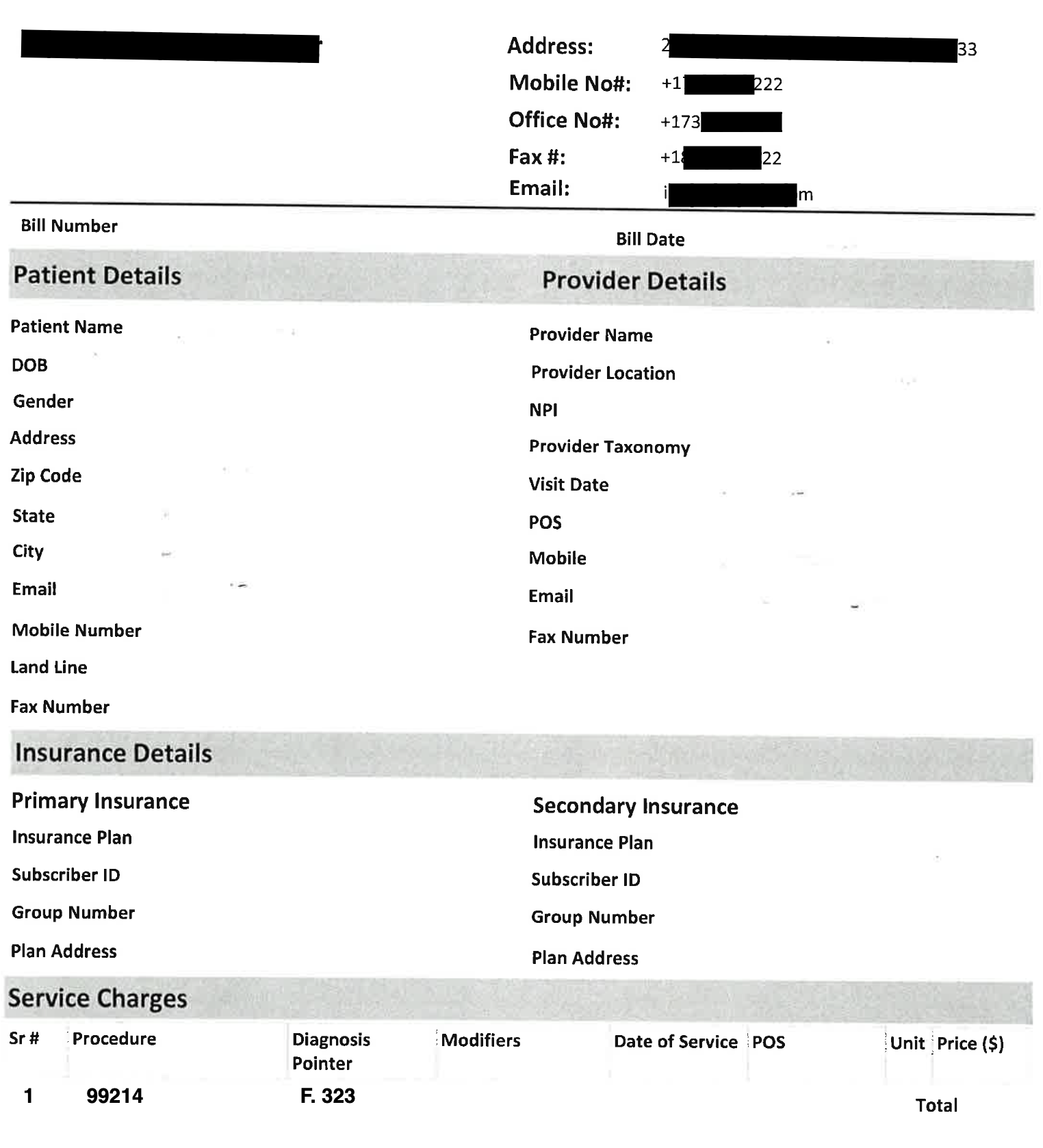

First, let’s name the key components of a superbill:

CPT-codes: The Current Procedural Terminology (CPT) code is a standardized way for healthcare providers to describe the specific services you received—like an initial evaluation or a therapy session—so your insurance company knows what was done and can process your claim accurately.

Diagnoses: Your diagnosis: Insurance companies need to understand why treatment was necessary, so a superbill includes an ICD code—this is the official diagnostic code that explains what you’re being treated for and helps confirm that the service was medically necessary.

Date of service: this is important for you to acknowledge when you’re filing your claims. It is paramount that you do not lapse in getting the paperwork to the insurance company. We recommend submitting 24-48 hrs after your visit to ensure our practice has enough time to troubleshoot any discrepancies and problems before your next appointment.

How do I get my Superbill?

In my practice, we send the superbill directly to our patient’s email. We are also able to provide them with a hard copy but that’s usually ready once I complete my documentation. In the end, your psychiatrist will determine how they want to give you the superbill. There might be a portal that can allow you to access & download a copy.

Does my Superbill contribute to my deductible?

Yes! Whenever you submit your claim, the insurance company will determine the allowable amount for each service –this will be counted towards your deductible. Once you reach your deductible, you’ll be responsible for paying a coinsurance on the allowable amount.

Let’s walk through an example of what an insurance reimbursement might look like for a psychiatrist visit:

1. Let’s say you paid $250 out of pocket for a 50-minute psychiatric session and submitted a superbill to your insurance.

2. Your insurer reviews the claim and says the Allowed Amount for that type of visit is $200—that’s the max they’ll consider for reimbursement.

This is a term that's typically quite confusing to patients. If you see a provider who is not in-network (as many providers are), even after meeting your deductible and out of pocket maximum, you will still be responsible for the cost of the visit above the Allowed Amount.

3. If you’ve already met your deductible: your plan might have a 30% coinsurance, meaning you’re responsible for $60. The remaining $140 would be reimbursed to you.

4. If you haven’t met your deductible yet: the insurance company will still process the claim and apply the $200 toward your deductible—but you won’t get any reimbursement just yet. You’re still responsible for the full $250 you paid, but you’re one step closer to hitting your deductible.

Hope this brings you some clarity in navigating insurance claims and superbill reimbursements. To summarize, a superbill is a detailed receipt I can provide for your sessions—it’s what you’ll need to request reimbursement from your insurance if I’m out-of-network. Your insurance company will process it based on your specific plan, so it’s a good idea to call them beforehand and ask how out-of-network mental health claims are handled. If a claim is denied, you usually have the option to appeal or resubmit. Not all providers offer superbills, so always double-check—without one, reimbursement isn’t possible.

More Articles

How Does Reimbursement Actually Work for Therapy / Psychiatry with Blue Cross Blue Shield in New Jersey?