Demystifying Insurance: Key Terms You Actually Need to Know

Crack the Code: Understand Your Health Insurance in Minutes

Let’s be real—health insurance can feel like a foreign language. Deductibles, coinsurance, claims... it’s a lot. In this post, we’re breaking it all down in plain English using real Blue Cross Blue Shield (BCBS) screenshots to guide you. Whether you’re new to insurance or just want to feel more in control of your care, you’re in the right place.

Many of our clients share how overwhelming insurance portals and paperwork can be, especially when you're trying to focus on your health. We're here to change that. So grab a coffee, open up your insurance portal, and let's walk through it together—step by step.

Know Your Insurance Categories

Psychiatric services (like therapy or medication management) fall under the Medical category of insurance. If you haven’t already, go ahead and log into your insurance portal—this post will make more sense if you can look at your own plan as we go.

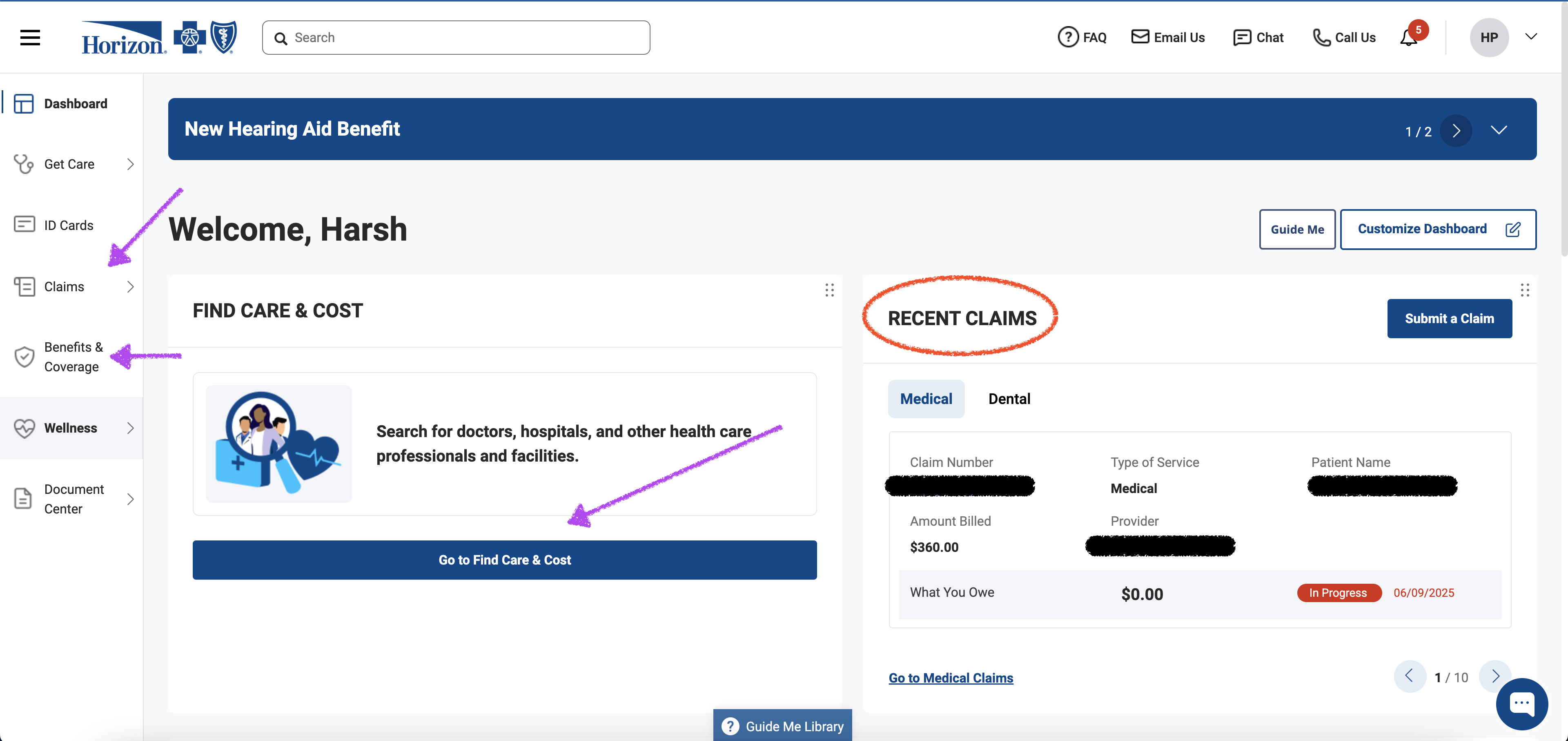

Get Familiar With Your Dashboard

Think of your insurance dashboard as your personal control panel. It’s where you’ll find everything from your policy details and benefit summaries to provider directories and hospital networks. You can also upload documents or view referrals here.

Explore Your Benefits & Coverage Page

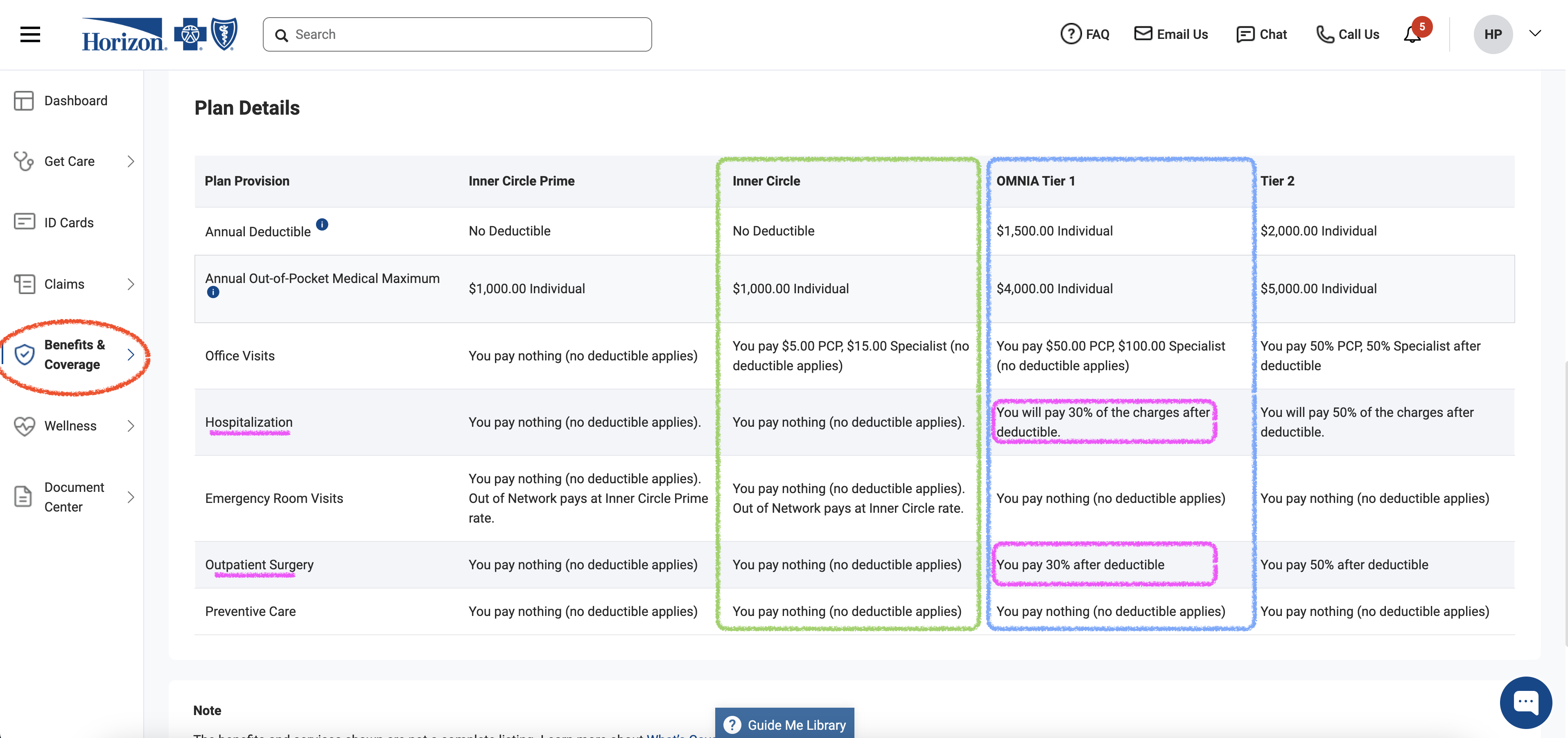

Once you’re inside your portal, click on Benefits & Coverage. In the example below, our patient has four active plans, but we’ll focus on comparing two: the Inner Circle plan and the OMNIA Tier 1 plan.

What Is Your Deductible

Deductible is the amount you pay out-of-pocket before your insurance starts covering services. It varies based on your specific plan and the provider network. Almost always, if the deductible is high, the monthly premium is low and vice versa. It is important to know your deductible factors into your total medical cost. You probably are familiar with this since it is something that can drastically change your monthly premium.

- Inner Circle Plan: This patient has no deductible. That means when they see a provider in-network, they only pay a copay—insurance covers the rest. These plans usually come with a higher monthly premium, but they offer excellent coverage and predictability.

- OMNIA Tier 1 Plan: This plan has a $1,500 deductible. Until the patient spends that amount, they’re responsible for all healthcare costs out of pocket.

Think of it like this: the deductible is your entry fee into full insurance coverage. Once you pay it, the real benefits begin.

Coinsurance: Your Share After the Deductible

Once your deductible is met, coinsurance kicks in. This is the percentage you pay for services, while insurance covers the rest.

For example:

- If your urgent care visit costs $1,000 and your plan has a 30% coinsurance, you’d pay $300, and insurance pays $700.

- Coinsurance usually applies to bigger-ticket items like hospital stays, surgeries, and specialist visits.

Copay is NOT coinsurance. Copay is a fixed fee assigned by insurance per plan – OMINA Tier 1 has a $50 copay for PCP and $100 for Specialists!

Out-of-Pocket Maximum: Your Yearly Safety Net

Here’s some good news: your expenses don’t go on forever. Every plan has an annual out-of-pocket maximum. This is the maximum amount you’ll pay in a year—including deductibles, coinsurance, and copays.

Once you hit that limit, your insurance covers 100% of covered services for the rest of the year. It’s your financial “ceiling,” and it’s there to protect you.

- Inner Circle Plan: This patient has an Out-of-Pocket Maximum of $1,000

- OMNIA Tier 1 Plan: This patient has an Out-of-Pocket Maximum of $4,000

Allowed Amount: The Secret Term that is Never Disclosed

However, even if you hit your Out-of-Pocket maximum, there is still an Allowed Amount that applies. If you see a provider who is Out of Network, the insurance company will decide on an amount for which the service can be reimbursed.

For example, if you see a psychiatrist whose charge for the service is $350, Blue Cross Blue Shield may only have an Allowed Amount of $120 for this type of service.

That means even after the deductible and out of pocket maximum are met, you will still be responsible for $230 of the $350 visit for every psychiatrist visit.

Insurance companies rarely list Allowed Amounts when patients are signing up for plans. If you're considering an insurance plan, try calling to get a better sense of what the Allowed Amount for different procedure codes are.

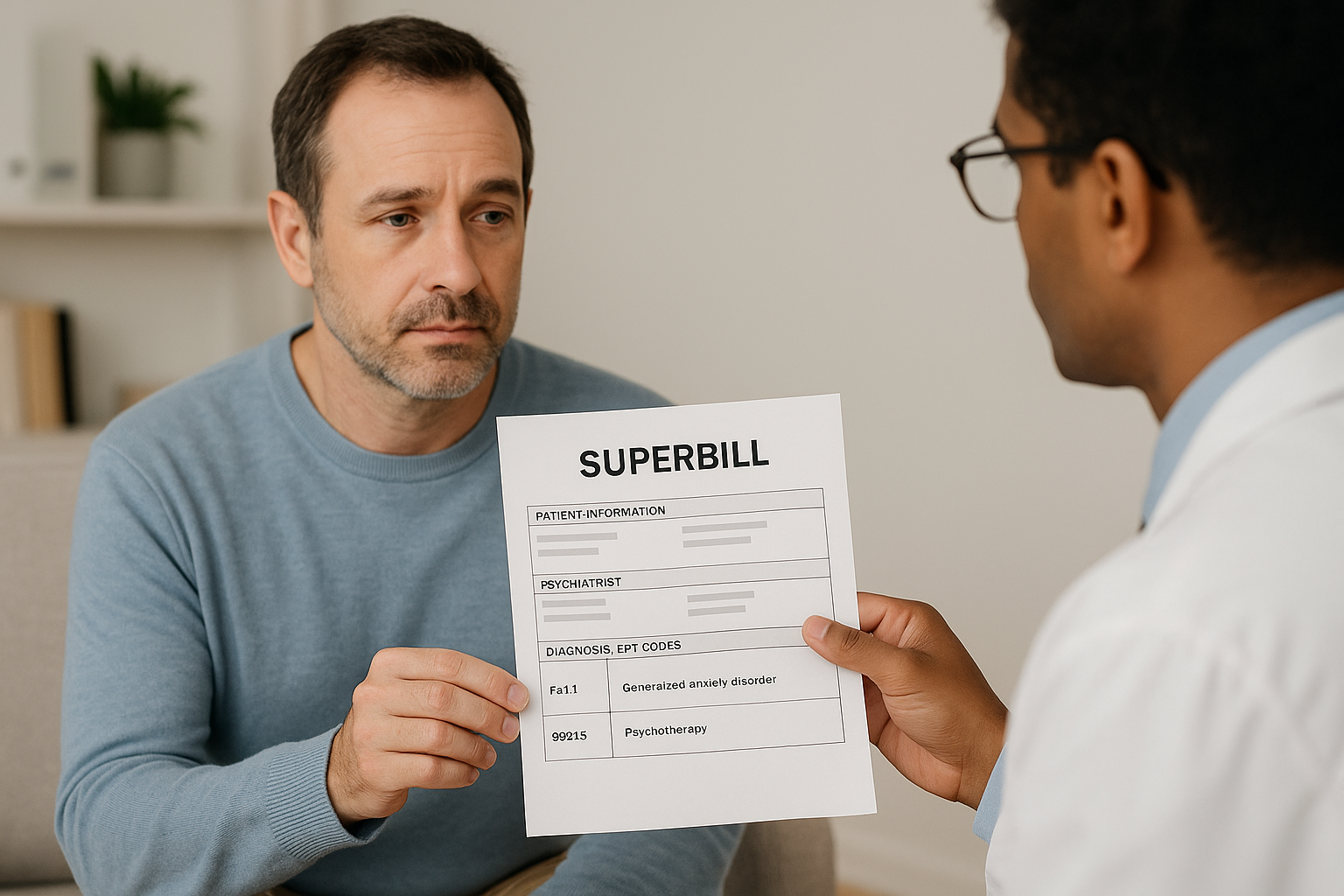

Claims: What They Are & Why They Matter

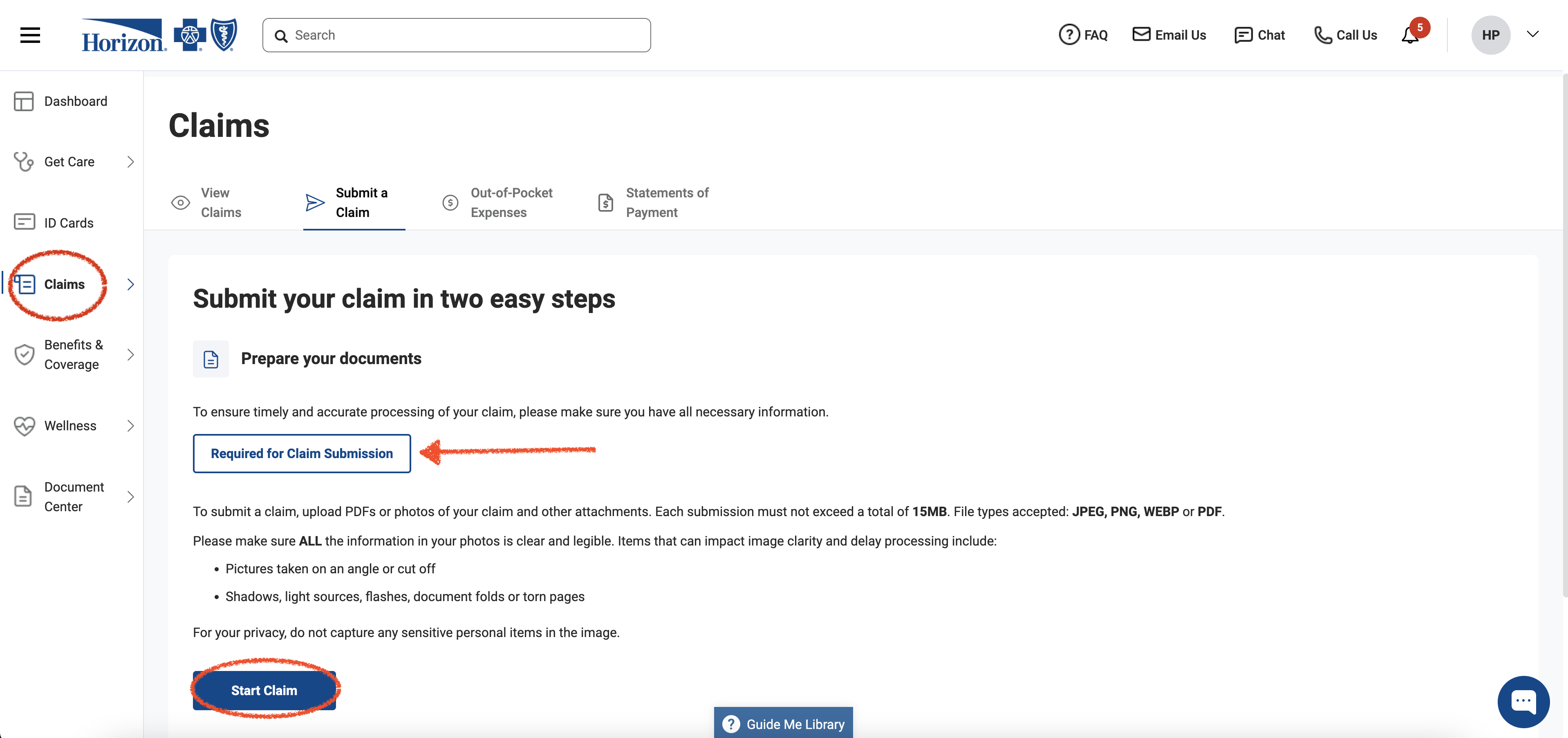

Lastly, one of the most important of it all – Claims! These are payment requests submitted to your insurance company. If you see an in-network provider, they’ll file claims on your behalf. For example, if you have a therapy session, the provider submits the claim to insurance, and the payment is handled between them.

If you see an out-of-network provider, you’ll need to submit the claim yourself for reimbursement. This sounds more intimidating than it is. Most insurance portals (like BCBS) have a step-by-step claims tab that walks you through what you need to upload—think receipts, dates of service, provider info, etc (Red Arrow below).

If you're ever stuck, your provider’s office manager can often help guide you through the process.

Still Feeling Stuck? Use These Tools.

There’s a lot of jargon in the insurance world. When you come across unfamiliar terms, check out your insurer’s Glossary page. It’s one of the best-kept secrets—quick definitions, real examples, and often links to helpful articles.

We also love this NPR podcast on navigating insurance that many of our clients have found helpful. It’s approachable and surprisingly entertaining.

To save you time, here are links to some major insurer glossary pages:

Blue Cross Blue Shield Horizon

More Articles

How Does Reimbursement Actually Work for Therapy / Psychiatry with Blue Cross Blue Shield in New Jersey?